In May 2006, Lynne Choate and her husband, Jesse, bought their Winslow home, appraised at $189,000, for a little more than $146,000.

With one child and two jobs, they applied for an adjustable rate mortgage, and thought they got a sweet deal: a 9.25 interest rate for the first two years, with no money down. In a year’s time, a representative told them the equity in their home would qualify them for a 3.5 percent interest rate.

Additional Photos

All was well for a while; the payment was a manageable $926 a month.

Then it all blew up. And the interest rate drop never came.

That October, the Choates’ payments ballooned to around $1,326 monthly.

In March 2009, they got their first default notice.

After periods of unemployment for both, the couple now takes in around $3,000 a month.

The Choates can’t afford their home.

They aren’t alone. As the foreclosure process grinds painfully forward across the country, a second wave of domestic pain is increasing the number of people in default, threatening neighborhoods with blight and putting an drag on an already fragile economic recovery.

Experts say the first wave of the foreclosure crisis snared homeowners in a spree of subprime lending; the second wave is from a persistently weak U.S. economy. The Choates are experiencing both.

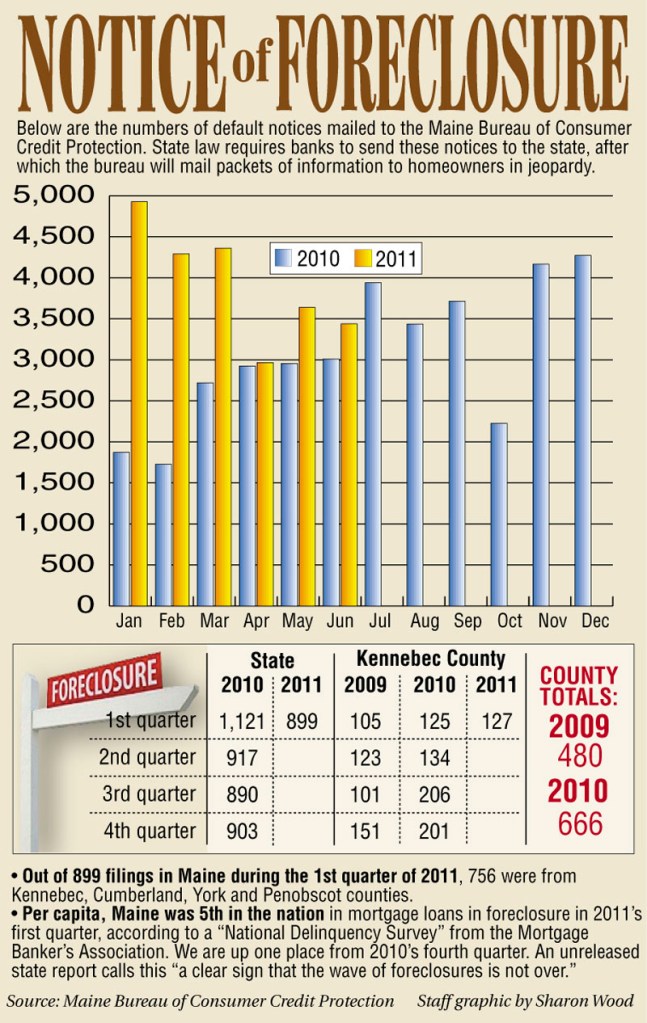

A forthcoming Maine Bureau of Consumer Credit Protection report says Maine ranked fifth in the nation in the first quarter of 2011 for number of homes in “foreclosure inventory” per capita, up from sixth place the previous quarter.

About 5.5 percent of all Maine homes are in this category. They are homes whose owners are at any point in the foreclosure process.

Of all Maine homes in the inventory, 8.26 percent, or 13,500 homes, are in “serious deliquency” — past 90 days in arrears.

The effect is drastic for the Choates. Electric bills have gone unpaid. Their vehicle was given up for voluntary repossession. And they face the prospect of being out in the street.

“We don’t take vacations,” said Lynne Choate, 35. “We don’t take trips. There are no extras.”

The mortgage has been flipped from firm to firm; Lynne Choate said she’s received default letters from five companies in the past three years.

A federal aid program rooted in an aggressive 2010 Wall Street reform law may be all that keeps the Choates from homelessness, and from putting another empty house back onto an oversupplied housing market.

But critics bristle at the notion that someone else’s personal financial woe should become the responsibility of taxpayers — or that the aid will solve, and not just delay, the country’s intractible foreclosure problem.

Easing the burden

Locally, the Bureau of Consumer Credit Protection said 14 percent of all Kennebec County households received a delinquency notice between June 2009 and January.

That only means lenders have started the process — comparatively few will be taken over by banks.

That’s low compared to some surrounding counties: Sagadahoc County was at approximately 23 percent during that period; with Lincoln, 18 percent; Somerset, 16 percent; and Androscoggin at 15 percent.

The 4,925 foreclosure notices sent to Maine homeowners in January was the most on record with the bureau.

So it’s likely the foreclosure rate will stay high nationally through at least 2014 and into 2015, the report says.

Lynne Choate was one of the first Mainers to apply for mortgage help through the the Emergency Homeowner Loan Program.

The program — authorized by the Dodd-Frank Wall Street Reform and Consumer Protection Act signed by President Obama in 2010 — grants selected homeowners a one-time forgivable loan to make mortgage payments, missed payments and late charges, up to $50,000 over a two-year period.

When that period is up, the homeowner is back on the hook. They also must meet with financial counselors a year into the program to make sure household budgets are sustainable.

The forgiveness of the loan comes after five years, only if homeowners have completely closed the gap on delinquent payments and remain the owner of the home.

Applicants must meet a long list of criteria. Among other things, they must be at least 90 days late on mortgage payment, have received a foreclosure notice and experienced a drop in income of at least 15 percent since 2009 from unemployment, underemployment or a medical condition.

Casey Bromberg — an administrator for the Kennebec Valley Community Action Program, which coordinates the program locally — said there were only 134 openings for aid initially.

But poor outreach nationally led to only 43,000 participants nationwide. That opened up waiting lists and put more than 200 more Mainers than expected into KVCAP’s application pipeline.

The small house where the program is based, next to KVCAP’s office in Waterville, is busier than usual right now. Intake for the program is extremely time-intensive. Documentation of each applicant’s financial situation can reach into the hundreds of pages.

Before a meeting, Bromberg told Lynne Choate — approximately six months and $15,000 behind on payments — she was “an early catch.”

“It doesn’t feel like it,” Choate responded.

‘Treated like criminals’

MaineToday Media was allowed access to the Choates’ financial records and a counseling meeting between Lynne Choate and KVCAP counselor Carol Homer.

In taking applicants through the process, the soft-spoken Homer, 64, said she often deals with upset, sometimes distraught, homeowners.

She had one just that day. “You’re lucky you weren’t here earlier,” she told Choate. “He was so mad at his mortgage company. I couldn’t calm him down. His wife eventually did.”

Homer also takes calls from bill collectors. With them, she talks a bit tougher.

Once, she said a client got a call from one of his lender’s collection agents, who asked him why he was working with KVCAP. The lender told the client that KVCAP was “only going to cause trouble.”

So Homer called the agent back.

“I said, ‘The only trouble we’re going to create is with you,'” she said. “Then I hung up.”

Homer reacts viscerally during a foreclosure interview, for good reason. She, too, has defaulted.

After being laid off in 2008, Homer said she took a temporary job at the veteran’s hospital in Togus, a 100-mile, three-hour round trip from her Cornville home.

When gas topped $4 a gallon, Homer said it was costing her a week’s salary to earn three weeks of pay.

“And that’s when I started to default,” she said.

Once she started making payments, Homer said she found out the holder of her mortgage was paying payments forward instead of backward, meaning they were still charging fees on missed payments.

Homer was able to get out from under impending foreclosure. But the experience, she said, makes her empathize with those who come into her office.

“It’s an attack on your way of life,” she said.

She rattled off another story of a widow she counsels being harassed by creditors for her late husband’s default.

“It’s breaking her heart. It’s dragging her down,” Homer said. “A lot of these people are hard-working Maine people. They’re good people.

“And they’re being treated like criminals.”

‘The inevitable’

The Emergency Homeowner Loan Program isn’t without its free-market detractors, including many in the housing industry.

Kennebec Savings Bank Executive Vice President Andrew Silsby believes such programs distort the housing market by prolonging imminent foreclosures. Others in the industry agree.

“You’re out working, and you keep things going, and there’s no help for you,” said Vernon Libby, a Farmingdale home appraiser. “I come along, and I’m behind, and I get a $50,000 loan?

“Do you think that’s the way to handle it?”

Bromberg responds quickly when she hears that criticism.

“I think that comes from a lack of knowledge about what the program does,” she said. “It catches people up.”

She said financial counseling after applicants enter the program creates a financial lifestyle change.

Meanwhile, Libby said he has seen an uptick in central Maine foreclosures in the past 30 months.

“About every 20 years, there’s some corrections,” he said. “But this is more than a correction. I have some serious concerns about our economy.”

U.S. housing prices peaked in 2006, according to a Bloomberg News report, but have steadily declined.

According to a RealtyTrac.com analysis, foreclosure filings in the United States exploded from about 885,000 in 2005 to 1,259,118 in 2006.

In 2007, then-Treasury Secretary Henry Paulson called the bursting housing bubble “the most significant current risk” to the country’s economy.

Then, from January to September 2008, nearly $900 billion in government money was earmarked to address the problem.

About $200 billion was injected into Fannie Mae and Freddie Mac, putting the longtime publicly traded, quasi-governmental, finance firms under conservatorship.

Other examples of federal largesse followed.

An $85 billion loan was given to insurance giant AIG, giving the government nearly an 80 percent stake in that company; $87 billion was given to major mortgage lender JPMorgan Chase.

By 2009, foreclosures rose to 2.3 million and 860,000 properties were repossessed, according to a January 2009 Associated Press report.

“It’s a shame the way the Fed has handled this,” Libby said. “They were telling banks, ‘You make that loan. If it goes sour, we’ll bail you out.'”

In 2010, the Frank-Dodd Wall Street Reform Act was signed by President Obama. The Emergency Homeowner Loan Program received approximately $3 billion in funding — $10.3 million originally in Maine.

Economists agreed the glut of foreclosed homes is driving prices down.

“Mainers think of ourselves as being savvy and conservative,” said William Lund, director of Maine Bureau of Consumer Credit Protection. “Maine consumers were swept up in the same enthusiasm to borrow as much as we could.”

Silsby said Kennebec Savings Bank holds roughly 7,000 mortgages worth $650 million, but doesn’t sell its notes to agencies such as Fannie Mae and Freddie Mac.

In 2008, he said, the bank handled no foreclosures. They still don’t handle many, he said — about 15 in 2009 and 2010 combined.

Whether it is this year or next, Silsby said, homeowners in tough mortgage situations likely will foreclose.

“In many cases, you’re delaying the inevitable,” he said.

Libby — while sympathetic — doesn’t believe programs such as the Emergency Homeowner Loan Program will make a dent in the nation’s foreclosure problem.

“If that’s going to keep the people in their houses and those people keep their jobs … then that might help the problem of foreclosures,” Libby said.

“I suspect all it will do is postpone the inevitable.”

MONDAY: The Choates anxiously await a decision on mortgage aid.

Michael Shepherd — 621-5662

mshepherd@mainetoday.com

Send questions/comments to the editors.

Comments are no longer available on this story